According to the "Q4 2024 Domestic Lodging Industry Trend Report" published by Yanolja Research (Director: SooCheong Jang), the domestic lodging industry experienced a decline in all accommodation types compared to the same period of the previous year and the previous quarter. The overall economic downturn, weakened consumer sentiment following the state of emergency, and seasonal winter factors combined to create this trend, with luxury accommodations seeing the most significant drop.

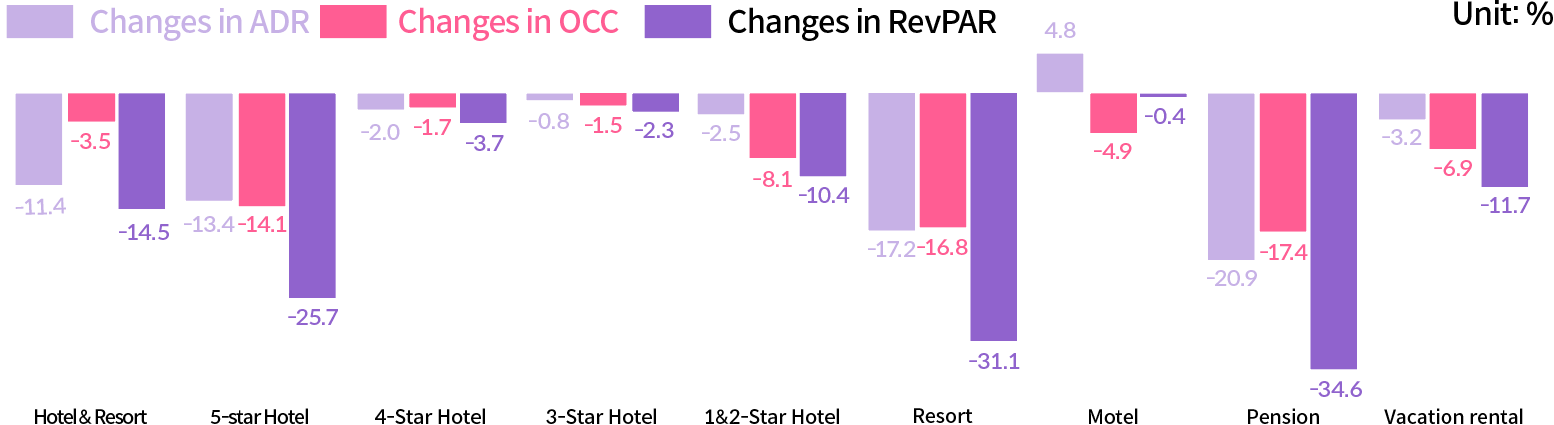

This report analyzes the overall domestic lodging industry for Q4 2024 based on data from Nol Universe, Airdna, and Yanolja Research’s proprietary survey. Key metrics analyzed include Average Daily Rate (ADR), Occupancy Rate (OCC), and Revenue Per Available Room (RevPAR). The report indicates that while RevPAR for 3-star and 4-star hotels declined by only 2.3% and 3.7%, respectively, RevPAR for 5-star hotels plummeted by 25.7%, marking a significant disparity. Additionally, due to the prolonged summer heat lasting until September, vacation demand was concentrated in Q3, severely impacting the pension and resort sectors in Q4. The OCC for pensions dropped by 6 percentage points, while resorts saw a 9.3% decline in OCC. RevPAR for pensions and resorts also recorded significant declines of 31.1% and 34.6%, respectively.

Changes in ADR/OCC/RevPAR by Accommodation Type (Q3 2024 vs. Q4 2024)

Performance Changes Compared to Q4 2023

In comparison to the same period in 2023, the overall performance of the domestic lodging industry declined in Q4 2024. The impact was most pronounced in luxury accommodations such as hotels and resorts, where ADR, OCC, and RevPAR all fell. ADR for 5-star hotels dropped by 8.8%, while resorts saw a 6.7% decline. OCC also decreased significantly, with a 23.9% drop for 5-star hotels and an 11.2% drop for resorts, indicating a decline in demand for high-end accommodations. RevPAR declined by 30.6% for 5-star hotels and 17.1% for resorts, further confirming the deteriorating performance.

Following the state of emergency in December 2024, the Bank of Korea’s Consumer Sentiment Index fell to 88, leading to a sharp decline in travel demand. The severe downturn in the luxury accommodation sector highlights the market's sensitivity, as these establishments rely heavily on year-end peak season demand.

On the other hand, mid-to-low-end accommodations such as motels, pensions, and shared accommodations saw relatively smaller declines. The RevPAR for motels and pensions decreased by 5.2% and 2.8%, respectively, while shared accommodations recorded only a 3.9% drop. This suggests that mid-to-low-end accommodations maintained demand due to their price competitiveness despite economic uncertainties.

Changes in ADR/OCC/RevPAR by Accommodation Type (Q4 2023 vs. Q4 2024)

Regional Performance: Severe Impact on Gangwon and Jeju

Regionally, major tourist destinations Gangwon and Jeju were hit hardest. RevPAR for 5-star hotels in Gangwon fell by 32.6% year-over-year, marking the largest decline nationwide. Jeju also saw a 41% quarter-over-quarter decline in resort RevPAR, reflecting a sharp deterioration in Q4 performance. This decline is attributed to a decrease in domestic air travel and limited accessibility to non-metropolitan areas.

Q1 2025 Outlook

The report also presents the "Lodging Business Outlook Index" for Q1 2025, indicating that the downturn in the hotel and motel sectors is expected to continue. The Lodging Business Outlook Index, published by Yanolja Research, is interpreted based on a baseline value of 100. An index above 100 suggests that more lodging operators expect improvement in the next quarter, while an index below 100 indicates a greater expectation of decline.

The ADR outlook index for hotels stood at 75.8, and the OCC outlook index was 74.2, both significantly below the baseline of 100. Motels also recorded an ADR outlook index of 84.9 and an OCC outlook index of 78.6, suggesting a continued slowdown compared to the previous year.

Suckwon Hong, Senior Researcher at Yanolja Research, stated,

"The 7-point decline in the prospective household spending index in December 2024 compared to the previous month indicates a weakening year-end consumer sentiment. This consumer sentiment slowdown is partially reflected in the Q1 2025 lodging business outlook index."

Long-term Development of the Lodging Industry: Expanding Inbound Tourism Through Regional Airport Activation

Additionally, the report emphasizes the importance of expanding inbound tourism for the sustainable growth of the domestic lodging industry, highlighting the need to improve accessibility to regional airports.

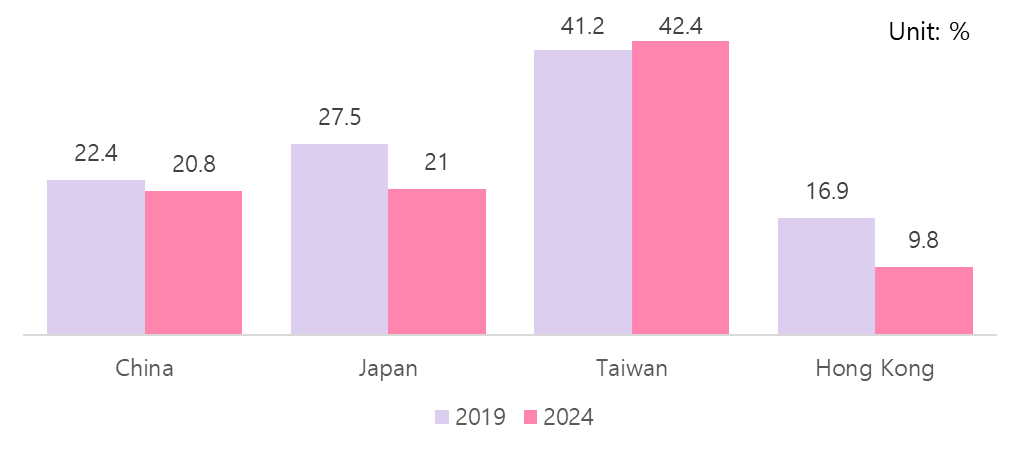

Analysis shows that among major Asian countries visiting South Korea, Taiwan was the only one to fully recover pre-pandemic visitor levels. Notably, there was a significant increase in non-metropolitan arrivals among Taiwanese tourists. From January to November 2024, the number of Taiwanese visitors entering metropolitan areas decreased by 5.1% compared to 2019 annual levels, while those arriving through Gyeongsang Province and Jeju increased by 15.9% and 92.3%, respectively.

Conversely, in 2024, the proportion of flights from China, Japan, and Hong Kong arriving at non-metropolitan airports in South Korea declined compared to 2019. However, flights from Taiwan to non-metropolitan airports increased, indicating a shift in Taiwanese travelers’ entry points from metropolitan to regional areas.

Commenting on this trend, Deachul Seo, Senior Researcher at Yanolja Research, stated,

"The Taiwanese case demonstrates that revitalizing regional airports can create new tourism demand. Promoting balanced regional development through this approach will be a key strategy for the long-term growth of the lodging industry."

Changes in the Proportion of Flights from China, Japan, Taiwan, and Hong Kong to Non-Metropolitan Airports in South Korea